Negative Liability Statement for Regular Taxpayers: Here’s What GSTR-3B Filers Need to Know

GSTR-3B filers should stay informed about these updates and be prepared to leverage the new facility for better tax management

GSTR-3B – GSTR-3B filing – GSTR-3B returns – GSTN Update – What is GSTR 3B – How to file GSTR 3B – taxscan

GSTR-3B – GSTR-3B filing – GSTR-3B returns – GSTN Update – What is GSTR 3B – How to file GSTR 3B – taxscan

The Goods and Services Tax Network ( GSTN ) has introduced a new facility that allows regular taxpayers to enter negative amounts in their GSTR-3B returns. Starting from the September GSTR-3B filing, taxpayers can now input negative amounts in the Outward Tax Liability section.

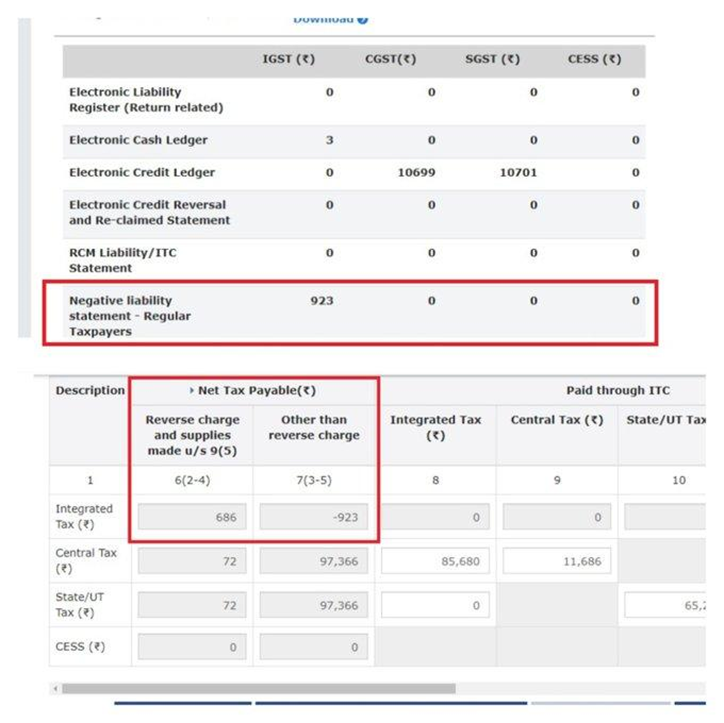

This is particularly beneficial for adjustments like credit notes or overpaid taxes in previous periods. Once the return is filed with a negative tax liability and the set-off is successful, the negative amount is transferred to a separate Negative Liability Statement. This amount can then be used to offset future tax liabilities under the same tax head when a positive liability arises.

Boost Your Business with SME IPO Funding Strategies - Enroll Now

This facility offers several benefits. It simplifies tracking by maintaining the negative balance separately on the portal, eliminating the need for taxpayers to manually keep track of negative liabilities awaiting future positive liabilities in the same head. Moreover, according to GSTR-3B rules, adjustments for one financial year previously had to be made by November 30 of the next financial year.

With this new feature, once the negative liability balance is created, it can be adjusted with future positive liabilities at any time in the future, as there is no time restriction.

However, there are some key observations to note. The negative liability has no relation to Input Tax Credit (ITC); it does not impact ITC and is only adjusted with future positive outward liabilities.

Boost Your Business with SME IPO Funding Strategies - Enroll Now

Additionally, negative liability created under one tax head will be used to offset positive liability in the same head. Cross-adjustment between different tax heads is not permitted.

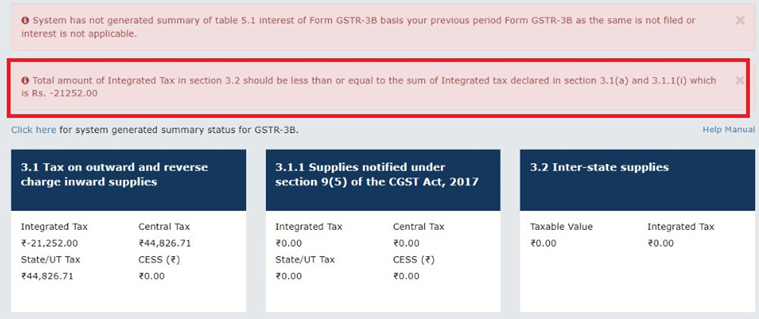

Currently, some issues have been reported on the portal. When a negative liability in IGST is entered in Table 3.1, the system throws an error stating that IGST in Table 3.2 cannot exceed IGST in Table 3.1. For example, if Table 3.1 has IGST as -₹923 and IGST in Table 3.2 is ₹0, the system displays an error.

Boost Your Business with SME IPO Funding Strategies - Enroll Now

It is vital to note that Table 3.2 entries are only for interstate supplies to unregistered persons or composition dealers, not B2B transactions. In the majority of cases, a negative liability of IGST arises due to B2B transactions, such as credit notes issued for sales returns or other reasons. Since these do not require entries in Table 3.2, the system should not throw this error.

The technical team at GSTN needs to urgently look into this matter, as the error is preventing many taxpayers from utilising this beneficial facility. Resolving this issue will enhance the user experience and ensure that the feature serves its intended purpose.

Boost Your Business with SME IPO Funding Strategies - Enroll Now

A Tax Consultant tweeted on twitter that, “We delayed our GSTR 3B filing due to this error and also raised grievance for the same, but the customer care team was also not able to solve the issue…”

In conclusion, the introduction of the Negative Liability Statement is a welcome move towards making tax compliance more flexible and taxpayer-friendly. It allows for efficient management of negative tax liabilities without the pressure of time constraints.

Support our journalism by subscribing to Taxscan premium. Follow us on Telegram for quick updates