West Bengal Govt implements DIN System on GST Communications to Taxpayers [Read Circular]

![West Bengal Govt implements DIN System on GST Communications to Taxpayers [Read Circular]](https://www.taxscan.in/wp-content/uploads/2023/04/West-Bengal-Government-DIN-System-DIN-GST-Communications-GST-Taxpayers-Taxscan.jpg "West Bengal Govt implements DIN System on GST Communications to Taxpayers [Read Circular]")

The West Bengal Government, in the Trade Circular 01/2023, dated 29.03.2023, announced the implementation of Generation and quoting of Document Identification Number (DIN) on communications issued under GST by the officers of the Directorate to tax payers and other concerned persons.

The Circular stated, “In keeping with the objectives of transparency and accountability in the administration of GST laws through widespread use of information technology, the Directorate of Commercial Taxes is implementing a system of electronic generation of Document Identification Number (DIN), hereinafter to be referred to as ‘WBGST DIN’, for those communications under GST that cannot be generated through GSTN portal, to be sent by the officers to the taxpayers or other concerned persons.”

“This measure would create a digital directory for maintaining a proper audit trail of such communications. Besides, it would provide the recipients of such communications a digital facility to ascertain the genuineness of such communications. Subsequently, WBGST DIN may be extended to other communications”, it was also added by the Commissioner of State Tax, West Bengal.

“Initially the WBGST DIN would be used for summons, arrest memos, search authorizations, inspection notices, recovery proceedings etc. as specified in para 5 of this Circular, relating to a taxpayer/ taxable person/any person, as the case may be”, the circular clarified.

The Trade Circular issued by the The Commissioner, in exercise of the power under section 168 of the West Bengal Goods and Services Tax Act, 2017, further directed that–

“All communications under the WBGST Act and rules made thereunder by officers, not below the rank of State Tax Officer of any Charge / Circle / Large Taxpayer Unit/ Unit or Zone of Bureau of Investigation, as the case may be, shall contain an electronically generated WBGST DIN from the online system of the Directorate of Commercial Taxes excepting in the following cases:-

when any such communication is made through the GSTN portal containing a unique reference number;

when any communication is made from the offices under the Directorate of Commercial Taxes other than any Charge/Circle/Large Taxpayer Unit/Unit or Zone under Bureau of Investigation;

when FORM GST MOV-01 and FORM GST MOV-02 are issued manually by the authorized officer who is outside the office while discharging his official duties.

WBGST DIN so generated shall be quoted prominently on the body of communications like summons, arrest memos, search authorizations, inspection notices, recovery proceedings and such other communications relating to a taxpayer/taxable person/any person, as the case may be;

when the communication is made by e-mail then the WBGST DIN shall be quoted on the body of the e-mail.

Notwithstanding anything mentioned in para 2 of this circular, in exceptional cases mentioned below, communications will be made without WBGST DIN:–

when there are technical difficulties in generation of WBGST DIN electronically; or

when communication regarding investigation/inquiry, verification etc. is required to be issued in short notice or in urgent situations and the authorized officer is outside the office while discharging his official duties:

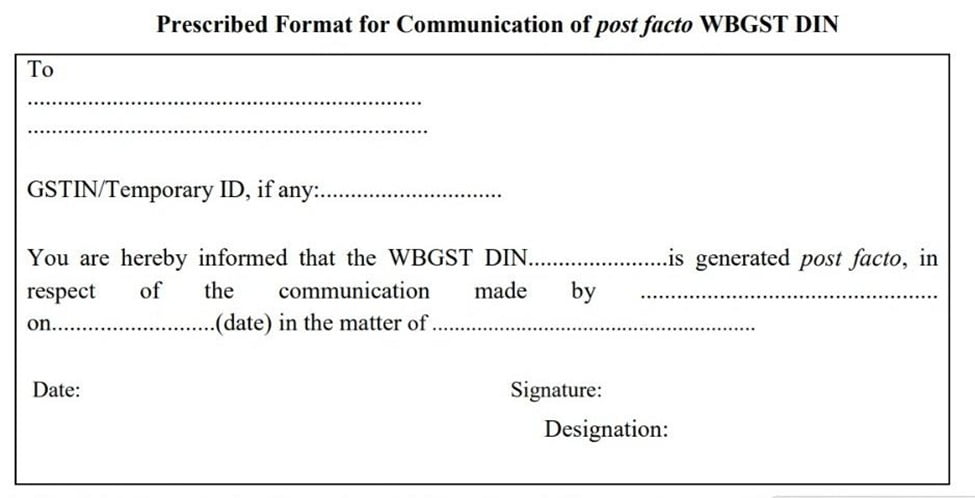

Provided that where the WBGST DIN could not be generated due to reasons specified in clause (a) above, the officer shall generate the corresponding WBGST DIN post facto within three working days from the date when such difficulties are overcome, and communicate such WBGST DIN to the recipient in the prescribed format given below.

Provided further that where the WBGST DIN could not be generated due to reasons specified in clause

(b) above, the officer shall generate WBGST DIN post facto within three working days from the date of issue of such communication and such WBGST DIN should also be communicated to the recipient in the prescribed format given below.

The Commissioner also directs that, subject to para 3 above, any communication, specified in para 2, which does not bear the electronically generated WBGST DIN shall be treated as invalid and shall be deemed to have never been issued.

The WBGST DIN will be generated for the following categories of communication, viz.,

i)Summons

ii)Arrest Memos

iii) Search authorisations

iv) Inspection notices

v) Other communications, such as:

Notice for return default

Notice for interest default

Notice for physical appearance

Notice/request against any mismatch for reconciliation

Intimation for recovery

Intimation for bank garnishee

Request for production of documents/ books of accounts

Any other communication

Structure of WBGST DIN issued by Directorate of Commercial Taxes, West Bengal: -

The structure is WBGST/1015/240123/023NNN (sample), where–

WBGST is common prefix,

The first digit 1 in 1015 stands for office type (can be either 1 for other offices or 2 for circles or 3 for charges),

The second, third and fourth digits 015 in 1015 stands for office code,

240123 stands for date of generation of WBGST DIN in DDMMYY format,

023 stands for serial number starting from 001 for a particular office and a particular date and NNN denotes 3-digit alpha-numeric system generated random number.

The genuineness of such communication can be ascertained by the recipient (taxpayer/ taxable person/any person) through the website of the Directorate of Commercial Taxes (Directorate of Commercial Taxes) using the WBGST DIN itself in the manner detailed below:–

DIN search page has a search field to type the WBGST DIN. After typing, the user needs to click on the “Search” button. In case of a valid WBGST DIN, the details of DIN, i.e., DIN status, DIN date (of generation) and name of the office where from the DIN was generated will be displayed. In the case of an invalid WBGST DIN, a message that “No data available in table” will be displayed.

This Trade Circular shall come into force with effect from 1st day of April, 2023.”

To Read the full text of the Circular CLICK HERE

Support our journalism by subscribing to Taxscan premium. Follow us on Telegram for quick updates

TRADE CIRCULAR No: 01/2023 , 29th March, 2023